Product Type

Your Guide to Financing Your Electrification Journey

Depending on the technology, financing can allow you to save money from day 1, even including loan repayments.

This guide provides a variety of different options for financing electric upgrades for those who can’t or don’t want to pay upfront. It contains general information only and is not financial advice. Everyone’s situation is different, so consider speaking with your bank or a licensed financial adviser before making a decision.

Why financing makes sense

Electric options for heating, hot water, cooking, and transport deliver significant savings over time because they are much cheaper to run.

Rather than waiting to save up money to cover the full upfront cost of the technolofoes, finance can unlock access right away.

Taking out loans can be viewed negatively, but it’s important to recognise that access to fair, low-cost finance is one of the key tools available to households to reduce costs and build long-term financial wellbeing, especially when it helps unlock savings that would otherwise be out of reach.

Example

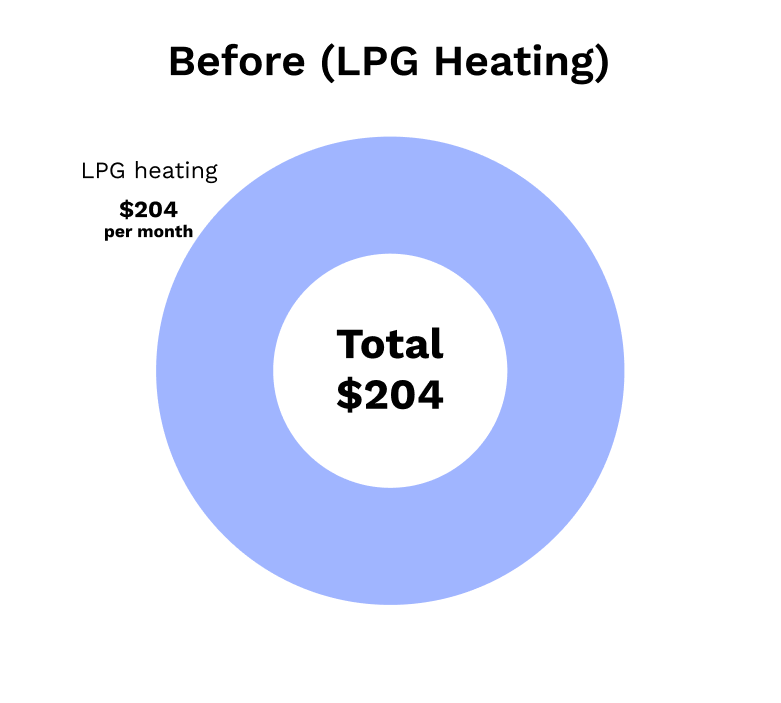

Tayla’s home is heated with LPG, which costs her around $2,450 a year to run. Ouch.

She’d love to switch to a heat pump, which would bring her heating costs down to about $500 a year, saving her nearly $2,000 every year, however she needs to find a way to afford the $3,800 upfront cost.

Tayla checks her options and finds she qualifies for a Green Loan through her bank (ANZ) with 1% interest over three years. She compares this to the other options available (home loan top up, personal loans and 0% credit), and decides this is the best option for her.

She goes ahead and takes out the loan. She then compares her previous and new monthly costs:

Before (LPG Heater):

LPG heating: $204 per month

Total monthly cost: $204

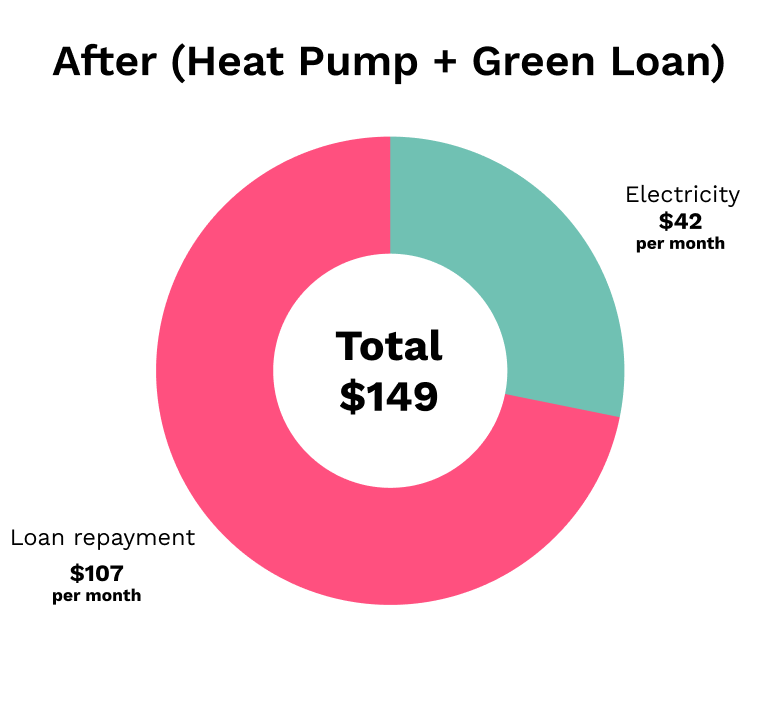

After (Heat Pump + Green Loan):

Electricity for heating: $42 per month

Loan repayment: $107 per month

Total monthly cost: $149

Even while repaying the loan, Tayla is $54 better off every month.

And after three years, once the loan is fully paid off, her monthly costs drop to just the electricity, meaning she’ll be around $162 better off every month from there on out.

An overview of finance options

.png)

Warmer Kiwi Homes Grant

Offers grants of 90% (up to $3,450) off heat pumps for eligible households.

-2.avif)

Bank Loans and Credit

Allow you to borrow money to pay upfront, then repay the loan over time with interest.

Ratepayer Assistance Scheme

The scheme, which is currently in development, will offer low interest, long term loans attached to rates payments.

The options available to you will depend on your specific financial situation and the type of product you are looking to buy. The table/tool below provides an overview of the different options covered in this guide and what type of electrification tech they cover.

If you are looking to finance an electric vehicle, visit MoneyHub’s EV Loans guide which includes financing options that are not covered on this page.

Select the electrifcation you would like finance for

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Interest Rates

Length of Term

Cooking

Heating

Hot Water

EV Vehicle

EV Charger

Solar

Batteries

Grants

Warmer Kiwi Homes

N/A, you don’t pay it back.

N/A, you don’t pay it back.

Green Home Loans

Kiwibank

Around 4.5% - 6%

10 years

Westpac

0%

5 years

ANZ

1%

3 years

ASB

1%

3 years

BNZ

1%

3 years

Bank Loans & Credit

Personal Loans

From 7%

Up to around 7 years

Credit (e.g. Cards)

0%

Up to 2 years

Home Loan Top Up

Around 4% - 6%

Length of mortgage (up to 30 years)

Other Loans

Ratepayer Assistance Scheme (Proposed 2026)

4% - 4.5% (assuming a 5.5% mortgage rate)

12 to 25 (aligned with the expected lifetime of the technology)

How to Choose The Right Finance Option

If we were you, we’d check eligibility for the Warmer Kiwi Homes grant (heat pumps only) before looking into bank loan options. If you’re eligible, it can help to lower the upfront cost and reduce the amount you need to borrow.

We’d then explore green loans, home loan top ups, personal loans and credit, and compare them using the Loan Calculator.

We’d also watch out for the Ratepayer Assistance Scheme, which may come out later in 2026 if it receives enough support.

The rest of this page goes into further details on each option and you can find further information in MoneyHub’s guide.

Option 1

Warmer Kiwi Homes Grant

The grant is offered by the Energy Efficiency and Conservation Authority (EECA) and targets low-income owner-occupiers. You may be eligible for a 90% grant for a heat pump (up to $3,450) if you have a Community Services Card, SuperGold Combo card, or live in the highest-need areas. That means you’ll pay only $400 to $700 for a heat pump. The grant also covers insulation.

Additional eligibility includes:

- The home was built before 2008.

- Have ceiling and underfloor insulation installed to EECA standards.

- Your home doesn't already have one of the following fixed heaters that is operational in any living area of the house: heat pump, wood or pellet burner, flued gas heater or central heating system.

Option 2

Bank Loans

Bank loans let you borrow money to pay for electrification technologies upfront, then repay the loan over time with interest. You own the technologies from day one. The types of loans available are:

- Green Loans: Offered by some banks for energy efficient upgrades, often with 0 to 1 percent interest.

- Home Loan Top Ups: General home improvement loans at your mortgage interest rate.

- Personal Loans/Credit: Unsecured and easier to access, but usually with higher interest rates.

-1.avif)

Which to choose?

Which options are available to you will depend on your financial situation. From there, choosing a finance option is a trade-off between what you can afford each month, what the upgrade costs you overall, and how much flexibility you want with your money.

- Options with higher monthly repayments can feel harder in the short term, but usually lead to lower total costs and higher lifetime savings.

- Options with lower monthly repayments are easier on the household budget, and leave more money available to save (or use elsewhere), but usually cost more in interest over time.

Even when the financial savings are smaller, electrification tech still deliver other benefits, such as more stable energy costs, improved comfort and performance, reduced emissions, and greater resilience when paired with solar.

There’s no single “best” option. The right choice depends on what matters most for your situation: lower monthly costs, greater flexibility, or maximising long-term savings. You can see how this plays out in the example further down the page.

Bank Loans

Green Loans

This type of loan is specifically for electrification and efficiency upgrades and most cover heat pumps, hot water heat pumps, solar, batteries, electric vehicles and electric vehicle chargers. Westpac’s green loan also includes cookers, and Kiwibank’s only includes solar and other generation technologies.

Green loans are often delivered as a home loan (mortgage) top-up, but with special rules and mostly lower interest rates.

Product

Interest Rates

Length of Term

Beyond the Initial Term

Borrowing Limit

1%

3 years

Move to other fixed loans or the floating rate.

$80,000

Mortgage rate: 4% - 6%

7 to 10 years

Move to other fixed loans or the floating rate.

N/A, but if you borrow more than $5,000 Kiwibank will contribute $2,000.

Benefits

- Very low or zero interest rates (much cheaper than a standard personal loan).

- Due to being short-term, the total interest paid is low

- Simple to apply for if you already have a home loan with that bank.

Considerations

- You need to hold your home loan with the bank.

- High monthly repayments (that may outweigh running cost savings depending on the technology), for the length of the term.

- Rates revert to higher, normal mortgage rates once the special green loan period ends.

- Requires a strong credit history, stable income and an acceptable debt-to-income ratio.

Bank Loans

Other Home Loan Top Ups

Most banks offer general home loan top ups. These are usually very flexible and allow you to use the funds on any home-related improvement or significant purchase. You can therefore use them on all electrification tech including electric vehicles and chargers.

This type of loan is added to your home loan at your agreed mortgage rate, and is therefore higher interest than green loans. In addition, even though the interest rate is lower than many shorter term personal loans, the long length of the repayment term can mean that the total cost of interest is much higher. But the economics really depend on how long is left on your home loan.

Reach out to your Home Loan provider to understand your eligibility and options.

Benefits

- Most banks offer this option, so they are more accessible than green loans.

- Allows you to make other home upgrades or renovations at the same time.

- More flexibility than green loans (covers induction hobs).

- Allows you to borrow more (sometimes the green loan limit isn’t high enough).

- Simple to apply for.

Considerations

- Higher interest rates compared to green loans reduce the savings made by switching to electric tech.

- Spreading the cost over more years increases the overall cost compared to shorter-term finance like personal loans.

- You need to hold your mortgage with the bank.

- Requires a strong credit history, stable income and an acceptable debt-to-income ratio.

Bank Loans

Personal Loans

Personal loans are another way to finance electrification upgrades. These loans are not tied to your property and normally come with higher interest rates (from around 7%) than home loan top up options. But they also have much shorter repayment periods (often up to 7 years), which somewhat limits how much interest you pay overall (compared to longer term loans).

You can use a personal loan for any electrification purchase including heat pumps, hot water systems, EV chargers, induction hobs, solar, batteries, and electric vehicles (though EVs sometimes require a specialised vehicle loan instead). You can view different options on MoneyHub’s Personal Loans page.

Benefits

- Shorter loan terms help keep total interest costs lower than a long home loan top-up.

- Can normally be used for any electrification technology.

- You don’t need to have a mortgage or own a home to access this option.

- Approval is relatively quick and simple.

Considerations

- Higher interest rates than mortgage-based finance options.

- Monthly repayments are higher because the loan term is shorter.

- Requires a good credit score and stable income.

- Interest rates can vary widely, so it pays to compare lenders.

Bank Loans

0% Interest Credit

Some banks offer credit cards with an introductory 0% interest period on purchases or balance transfers, often with a 2 to 24 month term. Credit limits are often around $5,000 - $7,500, which means they can be suitable for smaller electrification upgrades or covering part payment for more expensive upgrades.

Similarly, some installers offer promotional finance, often advertised as “interest free” for a fixed period (such as 6, 12, or 24 months). In many cases, this finance is provided through a third party lender and works in a similar way to a 0% credit card.

If the entire balance is repaid before the 0% period ends, these can be some of the cheapest financing options available. However, these options only work well if you are confident you can repay the balance in full within the interest free window. Once the promotion ends, they often revert to a much higher standard interest rate, such as 20 - 25% or more.

Benefits

- Can be effectively interest free if repaid within the promotional period.

- No need for a mortgage or property-secured loan.

- Very fast approval and quick access to funds.

- Useful for smaller electrification purchases (e.g., induction hobs, heat pumps, EV chargers) or part payment of larger ones.

- Installer finance can be convenient as it’s offered at the point of purchase.

Considerations

- High interest rates apply if the balance isn’t cleared in time.

- Lower credit limits may not cover larger upgrades like solar or batteries.

- Requires a good credit score to access, and can impact your credit score if mismanaged.

- Requires strong discipline to manage repayments.

- Installer finance terms vary so it’s important to check the fine print.

- Mostly suited to people who could afford to pay outright, but would like to take advantage of 0% interest.

Example Calculation

Financing an LPG Water Heater Replacement

Instead of replacing his LPG water heater with a like-for-like replacement, Tim is looking to upgrade to a heat pump hot water heater for $7,800. Although the upfront cost is higher than installing an LPG heater, the running costs are significantly lower.

Like-for-Like Replacement:

New LPG Water Heater: $3,400

Water Heating LPG Bill: $67 per month, $800 per year

Heat Pump Water Heater:

New Heat Pump Water Heater: $7,800

Water Heating Electricity Bill: $13 per month, $160 per year

Tim wants to access these savings but doesn't want to pay upfront, so he looks into his loan options using the Repayment Calculator.

Green Loan (1% interest over 3 years)

With this option, Tim’s repayments are high for the first three years. During that time, his monthly costs would be $13 for electricity (at current rates) plus $220 in loan repayments, totalling $233 per month. That’s $167 more than his current costs per month.

The upside is that the loan has low interest. Over the full term, Tim would only pay $121 in interest.

The total cost of the loan, including the principal and interest, is $7,921.

Home Loan Top Up (5% interest over 15 years)

In this option, the interest rate is 5% (Tim’s existing home loan interest rate) and the repayment term is 15 years (the duration left on his home loan).

The monthly payments are much lower than other loan options. He would pay $13 per month on electricity, and $62 on loan repayments, making $75 total. This provides a small monthly saving compared to what he is currently spending on LPG $67, so he knows it's affordable.

The total cost of the loan, including the principal and interest, is $11,103.

While this is higher than other options, it is still a better financial choice than sticking with LPG, and keeps Tim’s monthly outgoings close to what he pays today. This gives him more flexibility in the early years. He can keep that extra money in his pocket to save, invest, or use elsewhere, rather than putting it all into loan repayments upfront.

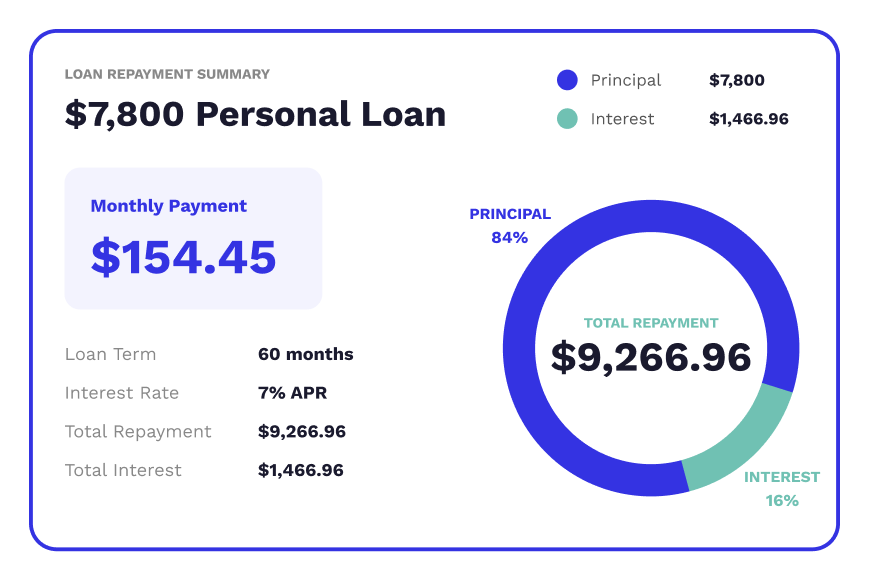

Personal Loan (7% interest over 5 years)

In this option, the interest rate is 7% (typical of a personal loan), and Tim has 5 years to pay it back.

Although the interest rate is higher than the green loan, the term is longer, so the monthly payments are less. He would pay $13 per month on electricity, and $154 on loan repayments, making $167 total.

Because the term is shorter than the home loan top up, the total interest paid is less at $1,467, making the total financing cost (with principal and interes $9,267.

While this option costs less than the home loan top up, it does mean higher costs in the early years of the system's life, leaving Tim with less money in his pocket to put towards other priorities.

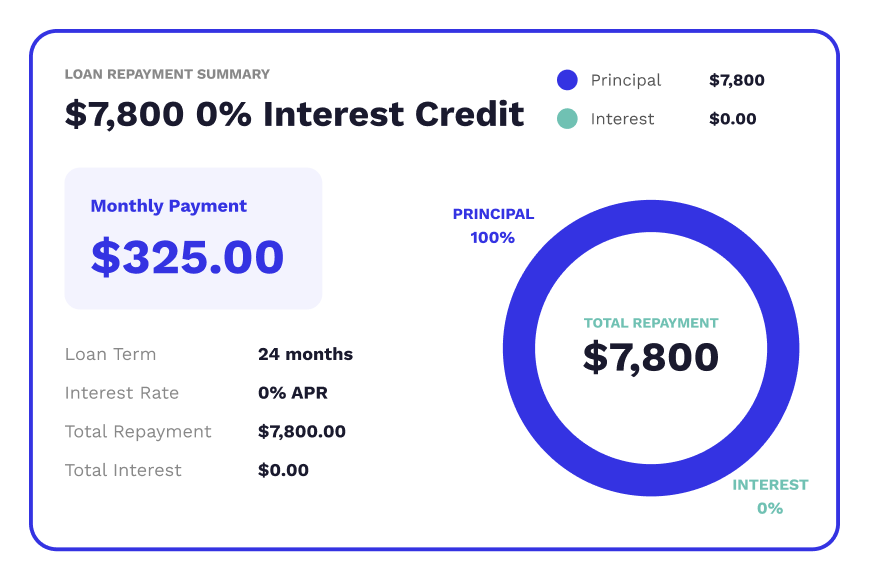

0% Interest Credit (0% over 2 years)

In this option, no interest is paid, but the two year term means the monthly repayments are very high. Tim would pay $13 per month on electricity, plus $325 in repayments, totalling $338.

Because there is no interest, the total is repayment is $7,800, but again, the initial higher costs leaves less in his pocket to grow in other ways.

This option would only be suitable if Tim is certain he can manage the high repayments and pay it off in full over the two years.

Summary of options

Green Loan

(1% over 3 years)

(1% over 3 years)

Home Loan Top Up

(5% over 15 years)

(5% over 15 years)

Personal Loan

(7% over 5 years)

(7% over 5 years)

0% Interest Credit

(0% over 2 years)

(0% over 2 years)

Total Monthly Cost (Electricity + Loan Repayments)

$233

$75

$167

$338

Total Interest Paid

$121

$3,330

$1,467

$0

Total Financing Cost

$7,921

$11,103

$9,267

$7,800

Outlook

✓ Low interest cost

✗ High monthly cost

✓ Lowest monthly cost, freeing up money to spend or save elsewhere

✗ Highest interest cost and total cost

✓ Lowest monthly cost of all the short term loans

✗ Highest total cost of all the short term loans

✓ No interest charged so has the lowest total cost

✗ Highest monthly cost

As mentioned, choosing a finance option is a trade-off between what is affordable each month, what the upgrade costs you overall, and how much flexibility you want with your money.

Tim will need to decide what is the most important to him - lower monthly payments and higher money flexibility, or lower total cost.

In this case, Tim chooses the home loan option because it delivers immediate savings from month one. His monthly costs decrease from $69 to $62, and frees up cash that he can put towards saving for other the electric technologies he has his eye on!

Watch this space!

Ratepayer Assistance Scheme

To make electric upgrades more accessible for everyone, Rewiring Aotearoa is supporting local councils (including Queenstown Lakes District Council) to develop a Ratepayers Assistance Scheme (RAS), which will hopefully become available in 2026.

Once introduced, the scheme will let you spread the cost of upgrades over time, typically 12 to 25 years (aligned with the lifetime of the technology). Instead of paying everything upfront, the repayments are added to your rates payments at an interest rate estimated to be around 1% to 1.5% lower than standard mortgage rates. The scheme is designed to make electrification more affordable for every rateable property in New Zealand by offering low-interest, long-term financing with flexible repayment options.

We need your help!

To make sure the RAS goes ahead, please sign our open letter where we are calling on the government to back the RAS.

Discover more resources

Solar Quote Comparison

Compare quotes side by side so you can see the best value for your home.

Household EV Guide

A step-by-step guide on everything you need to know before getting your first EV at home

Solar Step by Step Guide

Your easy roadmap to choosing the right solar setup for your home and budget.

-3.avif)

Solar Financing Guide

A clear breakdown of ways to pay for solar, from loans to grants, so you can pick what fits your situation.

.avif)

Solar for Renters Guide

Smart electrification tips for renters, including upgrades you can make without owning the place.

EV and Fleet Conversion

A straightforward guide to shifting your work vehicles to electric, with insights on savings and day to day operations.